Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

“Downward pricing pressure is likely to persist through the end of the year unless interest rates experience a significant decline. There was a 2-week uptick in buyer traffic and sales in September, as rates came down to the 6% range for conventional loans and 5.5% for VA & FHA loans. Since then, the rates have increased again.

Here are the basics – the ARMLS numbers for October 1, 2025 compared with October 1, 2024 for all areas & types:

- Active Listings: 24,450 versus 19,643 last year – up 25% – and up 5.2% from 23,238 last month

- Under Contract Listings (including Pending: 7,391 versus 7,261 last year – up 1.8% – and up 1.8% from 7,260 last month

- Monthly Sales: 6,141 versus 5,484 last year – up 12% – and up 3.6% from 5,928 last month

- Monthly Average Sales Price per Sq. Ft.: $287.14 versus $284.77 last year – up 0.8% – and up 2.2% from $280.97 last month

- Monthly Median Sales Price: $454,000 versus $442,000 last year – up 2.7% – and up 2.6% from $442,540 last month

September saw stronger demand thanks to lower interest rates, particularly during the first two weeks. Listings under contract rose 1.8% compared to a year earlier and sales closed during September were 12% higher than last year. However, this is partly because 2025 had one extra working day in September accounting for 5% of the difference.

Prices recovered from the decline they suffered over the previous 4 months and now stand higher than they did 12 months ago. However, some of that is because of a change in the sales mix, with luxury homes gaining ground over the last 4 weeks.

It is not all good news for sellers. Supply rose by over 5% over the past month and that upward trend looks likely to last until November at least. The surge in demand we saw starting in mid-August has largely petered out by the end of September as interest rates bounced back after the low point reached in mid-September. Source Cromford Report

| Why Oct. 12-18 might be the best week to buy a home |

Real estate experts say the week offers a rare trifecta—more listings, lower prices and less competition. “I expect this market momentum shift to magnify typical seasonal trends that favor home buyers in the fall,” says Danielle Hale, realtor.com®’s chief economist.

| Full Story: REALTOR® Magazine (9/17) |

Considering Buying or Selling? Let’s Connect.

With over 21 years of experience in the real estate market, I’m here to help you navigate your next move with confidence. Whether you’re looking to buy, sell, or simply explore your options, I’ll provide you with the insights you need to make informed decisions.

Even if you’re not planning to sell for several months, it’s never too early to start preparing. I offer personalized consultations where we can walk through your property together to identify improvements that can maximize your home’s value.

Curious About Your Home’s Value?

Click the Home Valuation link in my signature below for a comprehensive assessment.

Want to know more about your equity? I can also provide an Equity Analysis Report, which might reveal more value in your home than you realize.

Let’s chat soon to start planning your next move.

All the best,

SHAWN KEANE

REALTOR, ARIZONA

(602) 989-3209 Cell

shawn.keane@azmoves.com

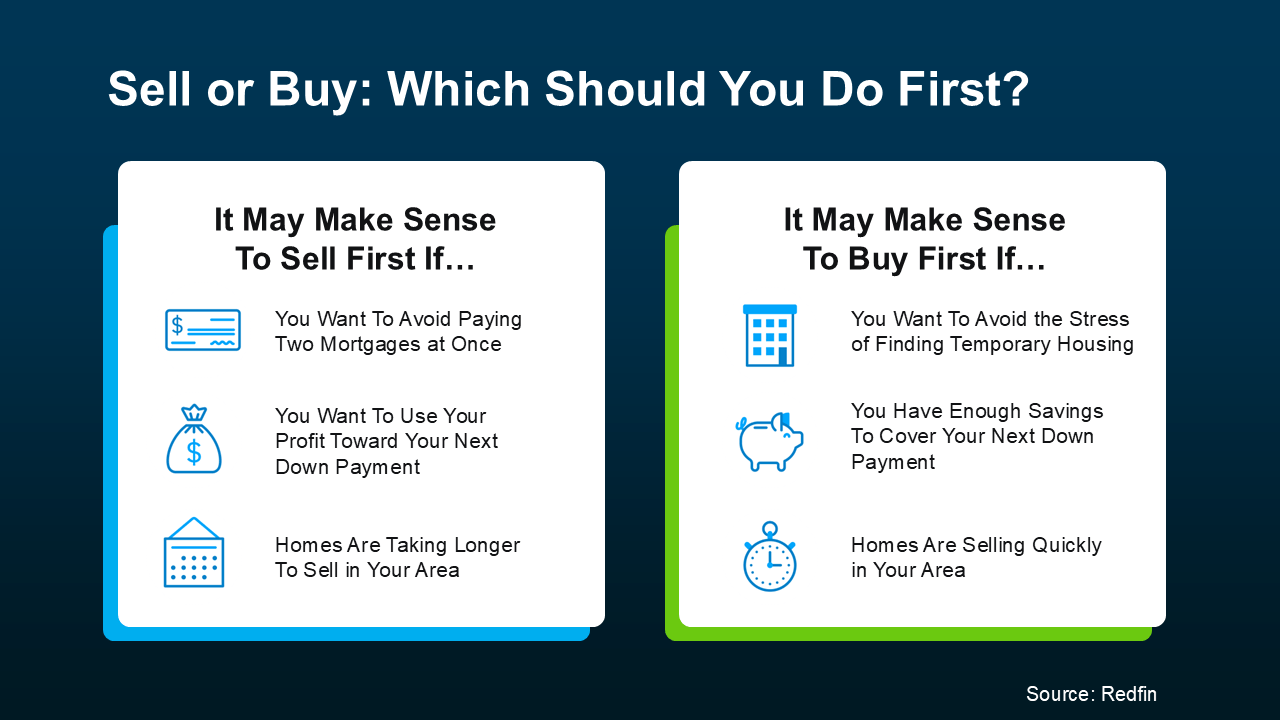

But the best way to determine what’s best for you and your specific situation? Talk to a trusted local agent.

But the best way to determine what’s best for you and your specific situation? Talk to a trusted local agent.