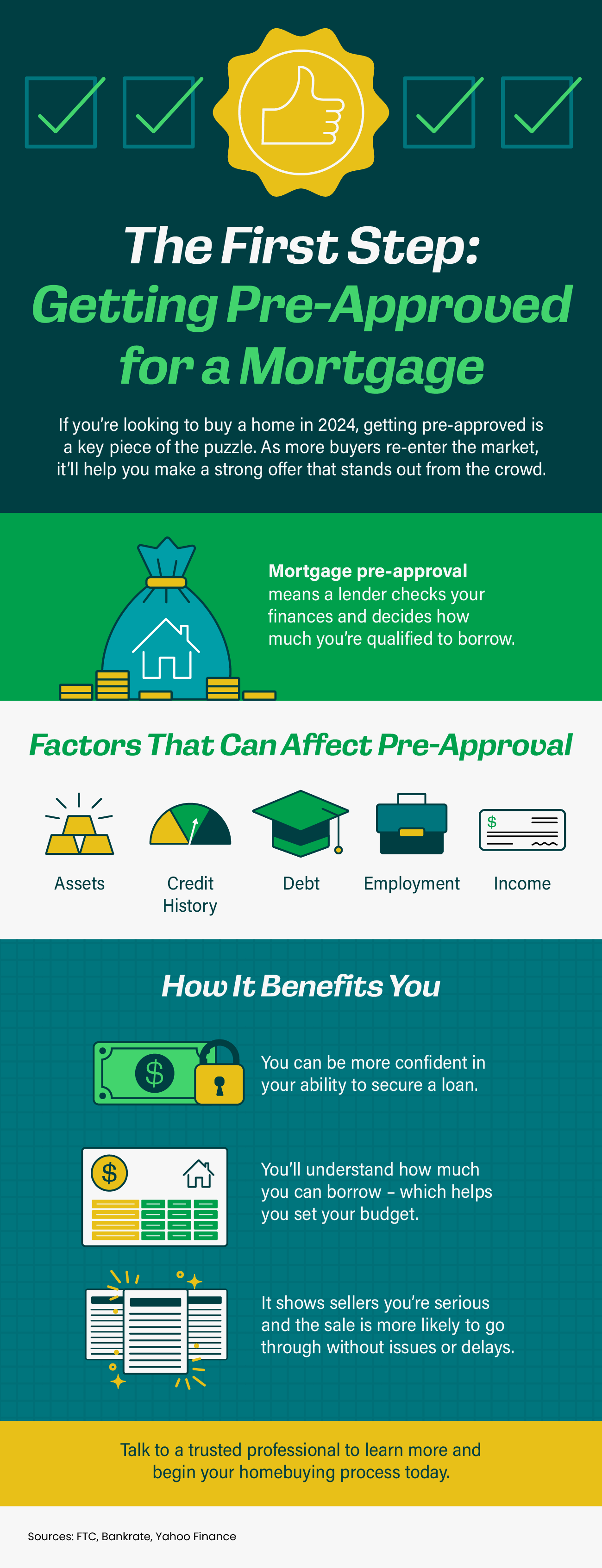

The First Step: Getting Pre-Approved for a Mortgage [INFOGRAPHIC]

Some Highlights

If you’re looking to buy a home in 2024, getting pre-approved is a key piece of the puzzle. Mortgage pre-approval means a lender checks your finances and decides how much you’re qualified to borrow.

As more buyers re-enter the market, it’ll help you make a strong offer that stands out from the crowd.

If you’re holding out hope that the housing market is going to crash and bring home prices back down, here’s a look at what the data shows. And spoiler alert: that’s not in the cards. Instead, experts say home prices are going to keep going up.

Today’s market is very different than it was before the housing crash in 2008. Here’s why.

It’s Harder To Get a Loan Now – and That’s Actually a Good Thing

It was much easier to get a home loan during the lead-up to the 2008 housing crisis than it is today. Back then, banks had different lending standards, making it easy for just about anyone to qualify for a home loan or refinance an existing one.

Things are different today. Homebuyers face increasingly higher standards from mortgage companies. The graph below uses data from the Mortgage Bankers Association (MBA) to show this difference. The lower the number, the harder it is to get a mortgage. The higher the number, the easier it is:

The peak in the graph shows that, back then, lending standards weren’t as strict as they are now. That means lending institutions took on much greater risk in both the person and the mortgage products offered around the crash. That led to mass defaults and a flood of foreclosures coming onto the market.

There Are Far Fewer Homes for Sale Today, so Prices Won’t Crash

Because there were too many homes for sale during the housing crisis (many of which were short sales and foreclosures), that caused home prices to fall dramatically. But today, there’s an inventory shortage – not a surplus.

The graph below uses data from the National Association of Realtors (NAR) and the Federal Reserve to show how the months’ supply of homes available now (shown in blue) compares to the crash (shown in red):

Today, unsold inventory sits at just a 3.0-months’ supply. That’s compared to the peak of 10.4 month’s supply back in 2008. That means there’s nowhere near enough inventory on the market for home prices to come crashing down like they did back then.

People Are Not Using Their Homes as ATMs Like They Did in the Early 2000s

Back in the lead up to the housing crash, many homeowners were borrowing against the equity in their homes to finance new cars, boats, and vacations. So, when prices started to fall, as inventory rose too high, many of those homeowners found themselves underwater.

But today, homeowners are a lot more cautious. Even though prices have skyrocketed in the past few years, homeowners aren’t tapping into their equity the way they did back then.

Black Knightreports that tappable equity (the amount of equity available for homeowners to access before hitting a maximum 80% loan-to-value ratio, or LTV) has actually reached an all-time high:

That means, as a whole, homeowners have more equity available than ever before. And that’s great. Homeowners are in a much stronger position today than in the early 2000s. That same report from Black Knight goes on to explain:

“Only 1.1% of mortgage holders (582K) ended the year underwater, down from 1.5% (807K) at this time last year.”

And since homeowners are on more solid footing today, they’ll have options to avoid foreclosure. That limits the number of distressed properties coming onto the market. And without a flood of inventory, prices won’t come tumbling down.

Bottom Line

While you may be hoping for something that brings prices down, that’s not what the data tells us is going to happen. The most current research clearly shows that today’s market is nothing like it was last time.

No matter how you slice it, buying or selling a home is a big decision. And when you’re going through any change in your life and you need some guidance, what do you do? You get advice from people who know what they’re talking about.

Moving is no exception. You need insights from the pros to help you feel confident in your decision. Freddie Macexplains it like this:

“As you set out to find the right home for your family, be sure to select experienced, trusted professionals who will help you make informed decisions and avoid pitfalls.”

And while perfect advice isn’t possible – not even from the experts, what you can get is the very best advice out there.

The Power of Expert Advice

For example, let’s say you need an attorney. You start off by finding an expert in the type of law required for your case. Once you do, they won’t immediately tell you how the case is going to end, or how the judge or jury will rule. But what a good attorney can do is walk you through the most effective strategies based on their experience and help you put a plan together. They’ll even use their knowledge to adjust that plan as new information becomes available.

The job of a real estate agent is similar. Just like you can’t find a lawyer to give you perfect advice, you won’t find a real estate professional who can either. That’s because it’s impossible to know everything that’s going to happen throughout your transaction. Their role is to give you the best advice they can.

To do that, an agent will draw on their experience, industry knowledge, and market data. They know the latest trends, the ins and outs of the homebuying and selling processes, and what’s worked for other people in the same situation as you.

With that expertise, a real estate advisor can anticipate what could happen next and work with you to put together a solid plan. Then, they’ll guide you through the process, helping you make decisions along the way. That’s the very definition of getting the best – not perfect – advice. And that’s the power of working with a real estate advisor.

Bottom Line

If you’re looking to buy or sell a home, you want an expert on your side to help you each step of the way. Let’s connect so you have advice you can count on.

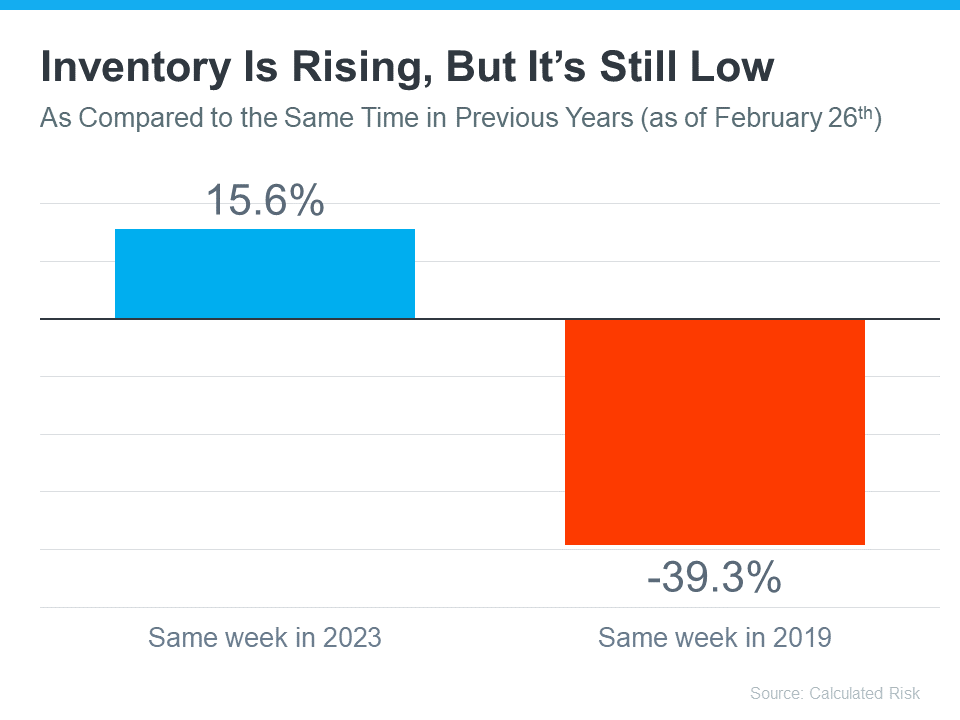

Why Today’s Housing Supply Is a Sweet Spot for Sellers

Wondering if it still makes sense to sell your house right now? The short answer is, yes. And if you look at the current number of homes for sale, you’ll see two reasons why.

An article from Calculated Risk shows there are 15.6% more homes for sale now compared to the same week last year. That tells us inventory has grown. But going back to 2019, the last normal year in the housing market, there are nearly 40% fewer homes available now:

Here’s a breakdown of how this benefits you when you sell.

1. You Have More Options for Your Move

Are you thinking about selling because your current house is too big, too small, or because your needs have changed? If so, the year-over-year growth gives you more options for your home search. That means it may be less of a challenge to find what you’re looking for.

So, if you were holding off on selling because you were worried you weren’t going to find a home you like, this may be just the good news you needed. Partnering with a local real estate professional can help you make sure you’re up to date on the homes available in your area.

2. You Still Won’t Have Much Competition When You Sell

But to put that into perspective, even though there are more homes for sale now, there still aren’t as many as there’d be in a normal year. Remember, the data from Calculated Risk shows we’re down nearly 40% compared to 2019. And that large a deficit won’t be solved overnight. As a recent article from Realtor.comexplains:

“. . . the number of homes for sale and new listing activity continues to improve compared to last year. However the inventory of homes for sale still has a long journey back to pre-pandemic levels.”

For you, that means if you work with an agent to price your house right, it should still get a lot of attention from eager buyers and could sell fast.

Bottom Line

If you’re a homeowner looking to sell, now’s a good time. You’ll have more options when buying your next home, and there’s still not a ton of competition from other sellers. If you’re ready to move, let’s connect to get the ball rolling.

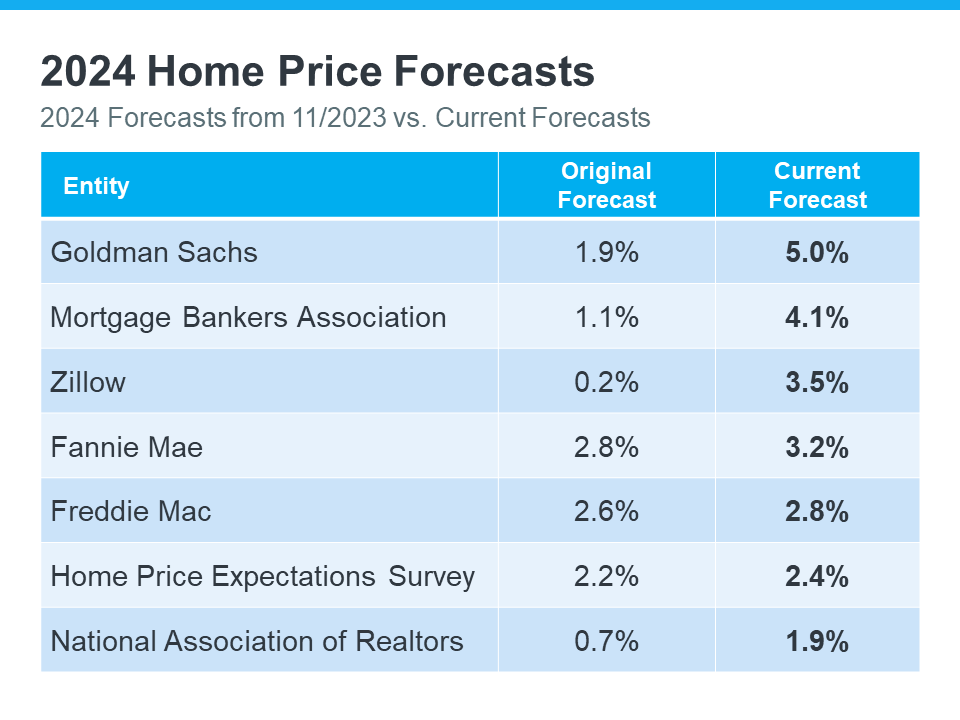

Over the past few months, experts have revised their 2024 home price forecasts based on the latest data and market signals, and they’re even more confident prices will rise, not fall.

So, let’s see exactly how experts’ thinking has shifted – and what’s caused the change.

2024 Home Price Forecasts: Then and Now

The chart below shows what seven expert organizations think will happen to home prices in 2024. It compares their first 2024 home price forecasts (made at the end of 2023) with their newest projections:

The middle column shows that, at first, these experts thought home prices would only go up a little this year. But if you look at the column on the right, you’ll see they’ve all updated their forecasts and now think prices will go up more than they originally thought. And some of the differences are major.

There are two big factors keeping such strong upward pressure on home prices. The first is how few homes are for sale right now. According to Business Insider:

“Low home inventory is a chronic problem in the US. This has generally kept home prices up . . .”

A lack of housing inventory has been pushing prices up for a long time now – and that’s not expected to change dramatically this year. But what has changed a bit is mortgage rates.

Late last year when most housing market experts were calling for home prices to rise only a little bit in 2024, mortgage rates were up and buyer demand was more moderate.

Now that rates have come down from their peak last October, and with further declines expected over the course of the year, buyer demand has picked up. That increase in demand, along with an ongoing lack of inventory, is what’s caused the experts to feel the upward pressure on prices will be stronger than they expected a couple months ago.

A Look Forward To Get Ahead of the Next Forecast Revisions

Real estate experts regularly revise their home price forecasts as the housing market shifts. It’s a normal part of their job that ensures their projections are always up-to-date and factor in the latest changes in the housing market.

That means they’ll continue to revise their projections as the housing market changes, just as they’ve always done. How those forecasts change next is anyone’s guess, but pay attention to mortgage rates.

If they trend down as the year goes on, as they’re expected to do, that could lead to more buyer demand and even higher home price forecasts.

Basically, it’s all about supply and demand. With supply still so limited, anything that causes demand to go up will likely cause prices to go up, too.

Bottom Line

At first, experts believed home prices would only go up a little this year. But now, they’ve changed their minds and forecast prices will grow even more than they originally thought. Let’s connect so you know what to expect with prices in our area.

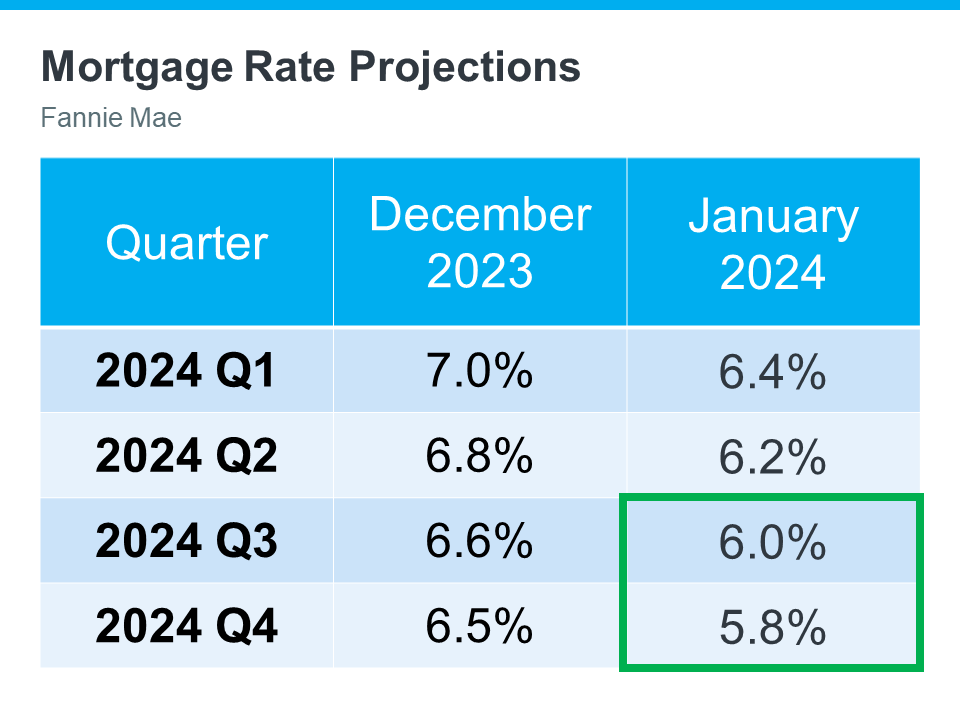

Some Experts Say Mortgage Rates May Fall Below 6% Later This Year

There’s a lot of confusion in the market about what’s happening with day-to-day movement in mortgage rates right now, but here’s what you really need to know: compared to the near 8% peak last fall, mortgage rates have trended down overall.

And if you’re looking to buy or sell a home, this is a big deal. While they’re going to continue to bounce around a bit based on various economic drivers (like inflation and reactions to the consumer price index, or CPI), don’t let the short-term volatility distract you. The experts agree the overarching downward trend should continue this year.

While we won’t see the record-low rates homebuyers got during the pandemic, some experts think we should see rates dip below 6% later this year. As Dean Baker, Senior Economist, Center for Economic Research, says:

“They will almost certainly not fall to pandemic lows, although we may soon see rates under 6.0 percent, which would be low by pre-Great Recession standards.”

And Baker isn’t the only one saying this is a possibility. The latest Fannie Mae projections also indicate we may see a rate below 6% by the end of this year (see the green box in the chart below):

The chart shows mortgage rate projections for 2024 from Fannie Mae. It includes the one that came out in December, and compares it to the updated 2024 forecast they released just one month later. And if you look closely, you’ll notice the projections are on the way down.

It’s normal for experts to re-forecast as they watch current market trends and the broader economy, but what this shows is experts are feeling confident rates should continue to decline, if inflation cools.

What This Means for You

But remember, no one can say for sure what will happen (and by when) – and short-term volatility is to be expected. So, don’t let small fluctuations scare you. Focus on the bigger picture.

If you’ve found a home you love in today’s market – especially where finding a home that meets your budget and your needs can be a challenge – it’s probably not a good idea to try to time the market and wait until rates drop below 6%.

With rates already lower than they were last fall, you have an opportunity in front of you right now. That’s because even a small quarter point dip in rates gives your purchasing power a boost.

Bottom Line

If you wanted to move last year but were holding off hoping rates would fall, now may be the time to act. Let’s connect to get the ball rolling.

Here are the basics – the ARMLS numbers for February 1, 2024 compared with February 1, 2023 for all areas & types:

Active Listings: 15,574 versus 15,598 last year – down 0.2% – but up 7.1% from 14,543 last month

Pending Listings: 4,576 versus 5,109 last year – down 10.4% – but up 40% from 3,263 last month

Under Contract Listings (including Pending, CCBS & UCB): 7,423 versus 7,810 last year – down 5.0% – but up 45% from 5,127 last month

Monthly Sales: 4,397 versus 4,350 last year – up 1.1% – but down 10.8% from 4,928 last month

Monthly Average Sales Price per Sq. Ft.: $288.95 versus $267.73 last year – up 7.9% – and up 1.4% from $284.89 last month

Monthly Median Sales Price: $430,000 versus $410,000 last year – up 4.9% – but almost unchanged from $429,990 last month

This is a mixed picture. Closed listing counts remain desperately low at 4,397 per month, only up 1.1% from this time last year. However, the number of listings under contract is growing nicely, up 45% from the dismal count at the start of the year. This is slightly better than the 43% we saw a year ago but not enough to signal a dramatic change in mood among buyers. We always expect to see strong growth between January and February and the observation in 2024 is middle-of-the-road.

A year ago, the Cromford® Report was markedly more positive about the market than the general sentiment, with many people unwisely predicting a market crash. There is still no sign of a market crash in the short or medium term, but the big difference between this year and 2023 is the strengthening of the incoming supply. We have seen almost 20% more new listings year-to-date than we did in 2023. Many pundits tend to focus almost exclusively on demand and were dismayed by the weakness in demand 12 months ago. However supply is equally important and many of these same pundits failed to notice that unusually weak supply was the key issue in early 2023. That weakness has evaporated and although the active listing counts are still low by long-term standards, they are looking much healthier than last year. The number of active listings without a contract is up 7.1% over the last month. Last year they went down 4.3%. This is a significant difference.

It is always good for a seller to have less competition from other homes. In some price ranges, the competition has increased dramatically since the start of the year, but in others it has barely changed at all.

Single-family active listings priced at $2 million or above have increased by 28% over the last month, rising to 951. This is unusual.

Single-family active listings priced between $500,000 and $2 million have seen an increase of 8%, rising to 5,438. This is normal for the time of year.

Single-family active listings priced below $500,000 have seen a fall of 0.2% to 4,505. This means the low-end of the market is still experiencing tight supply.

Prices are up by almost 8% from this time last year when measured by average $/SF. They are up almost 5% if measured by median sales price. Home prices are up by more than the Consumer Price Index. Market crash forecasters got this completely wrong, and buyers who followed their advice to wait have made a costly mistake.

Volume remains weak but the overall market is still tilted slightly in favor of sellers, with the Cromford® Market Index stable around 117 to 118. This tilt towards sellers is weakening in the upper price ranges, however. Buyers with more than $2 million to spend are probably thinking about flexing their negotiating muscles.

Did you know that Scottsdale ranks # 1 among best cities for jobs in the US. Read article here:

Go to my website for up-to-date information and a special feature called “Neighborhood News” “the best way to stay connected to what’s happening in the real estate market in your area”. See homes that are for sale and recently sold, find out if home sales in your neighborhood are trending up or down, see what homes around you are currently selling for. Also, you can search real time listings in any area of the market under (Find Your Dream Home.) Check it out and stay updated with my daily blog and monthly market report that I send out monthly. My Website–Find Your Dream Home

If you’re considering selling or buying, give me a call to discuss your situation and current market conditions.

The best compliment is a referral to your family and friends!

Over the past year, a lot of people have been talking about housing affordability and how tight it’s gotten. But just recently, there’s been a little bit of relief on that front. Mortgage rates have gone down since their most recent peak in October. But there’s more to being able to afford a home than just mortgage rates.

To really understand home affordability, you need to look at the combination of three important factors: mortgage rates, home prices, and wages. Let’s dive into the latest data on each one to see why affordability is improving.

1. Mortgage Rates

Mortgage rates have come down in recent months. And looking forward, most experts expect them to decline further over the course of the year. Jiayi Xu, an economist at Realtor.com, explains:

“While there could be some fluctuations in the path forward … the general expectation is that mortgage rates will continue to trend downward, as long as the economy continues to see progress on inflation.”

And even a small change in mortgage rates can have a big impact on your purchasing power, making it easier for you to afford the home you want by reducing your monthly mortgage payment.

2. Home Prices

The second important factor is home prices. After going up at a relatively normal pace last year, they’re expected to continue rising moderately in 2024. That’s because even with inventory projected to grow slightly this year, there still aren’t enough homes for sale for all the people who want to buy them. According to Lisa Sturtevant, Chief Economist at Bright MLS:

“More inventory will be generally offset by more buyers in the market. As a result, it is expected that, overall, the median home price in the U.S. will grow modestly . . .”

That’s great news for you because it means prices aren’t likely to skyrocket like they did during the pandemic. But it also means it’ll probably cost you more to wait. So, if you’re ready, willing, and able to buy, and you can find the right home, purchasing before more buyers enter the market and prices rise further might be in your best interest.

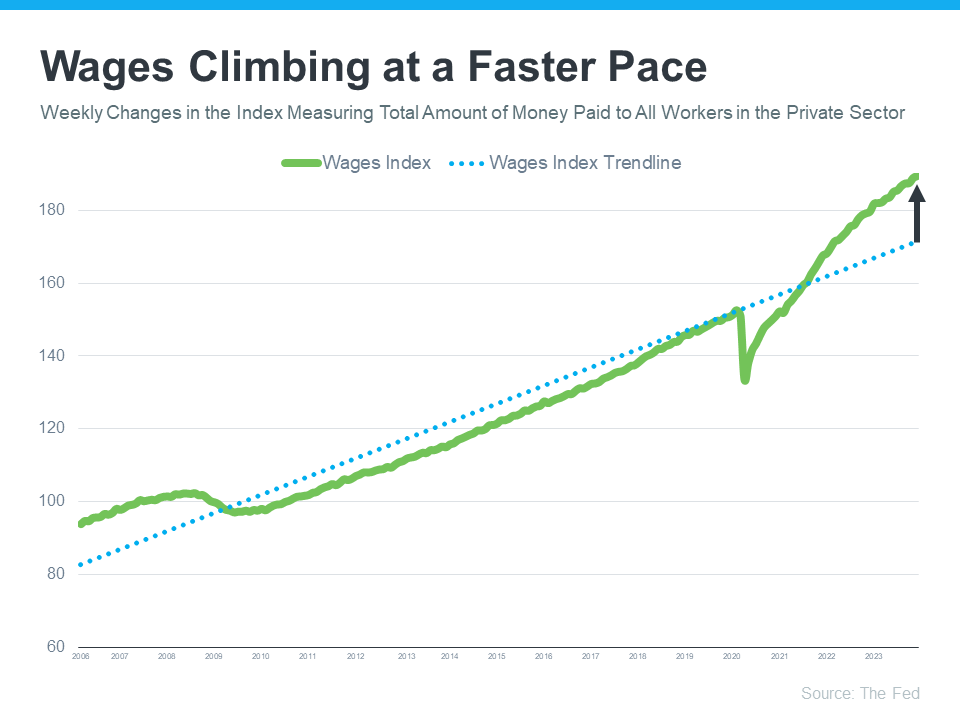

3. Wages

Another positive factor in affordability right now is rising income. The graph below uses data from the Federal Reserve to show how wages have grown over time:

If you look at the blue dotted trendline, you can see the rate at which wages typically rise. But on the right side of the graph, wages are above the trend line today, meaning they’re going up at a higher rate than normal.

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage. That’s because you don’t have to put as much of your paycheck toward your monthly housing cost.

What This Means for You

Home affordability depends on three things: mortgage rates, home prices, and wages. The good news is, they’re moving in a positive direction for buyers overall.

Bottom Line

If you’re thinking about buying a home, it’s important to know the main factors impacting affordability are improving. To get the latest updates on each, let’s connect.

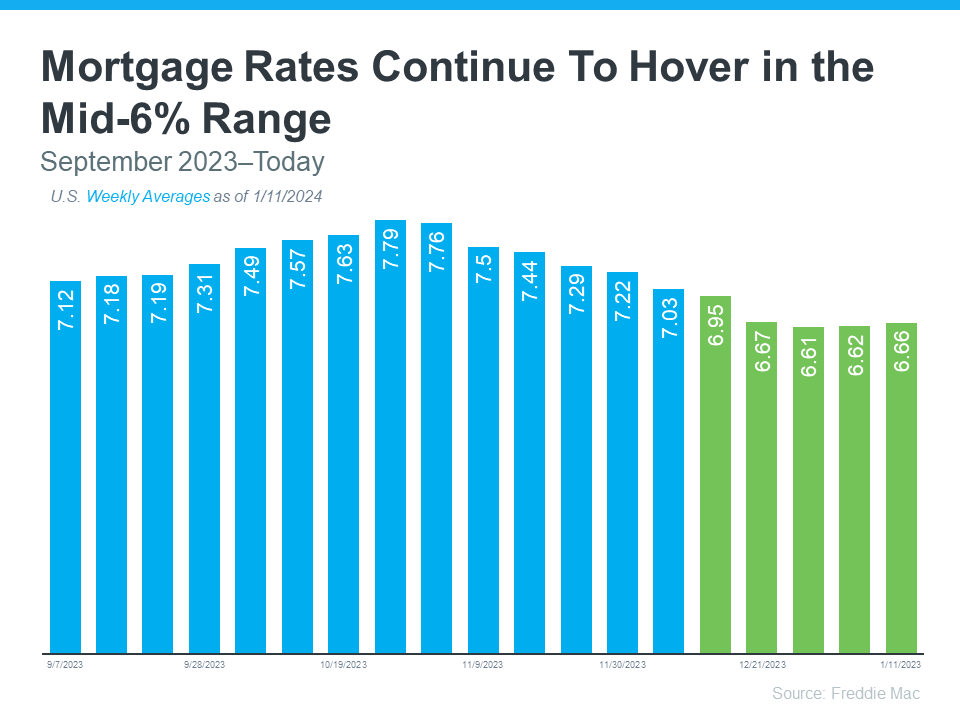

2 Reasons Why Today’s Mortgage Rate Trend Is Good for Sellers

If you’ve been holding off on selling your house to make a move because you felt mortgage rates were too high, their recent downward trend is exciting news for you. Mortgage rates have descended since last October when they hit 7.79%. In fact, they’ve been below 7% for over a month now (see graph below):

And while they’re not going back to the 3% we saw during the ‘unicorn’ years, they are expected to continue to go down from where they are now in the near future. As Dean Baker, Senior Economist at the Center for Economic Research, explains:

“It also appears that mortgage rates are now falling again. They will almost certainly not fall to pandemic lows, although we may soon see rates under 6.0 percent, which would be low by pre-Great Recession standards.”

Here are two reasons why this recent trend, and the expectation it’ll continue, is such good news for you.

You May Not Feel as Locked-In to Your Current Mortgage Rate

With mortgage rates already significantly lower than they were just a few months ago, you may feel less locked-in to the current mortgage rate you have on your house. When mortgage rates were higher, moving to a new home meant possibly trading in a low rate for one up near 8%.

However, with rates dropping, the difference between your current mortgage rate and the new rate you’d be taking on isn’t as big as it was. That makes moving more affordable than it was just a few months ago. As Lance Lambert, Founder of ResiClub, explains:

“We might be at peak “lock-in effect.” Some move-up or lifestyle sellers might be coming to terms with the fact 3% and 4% mortgage rates aren’t returning anytime soon.”

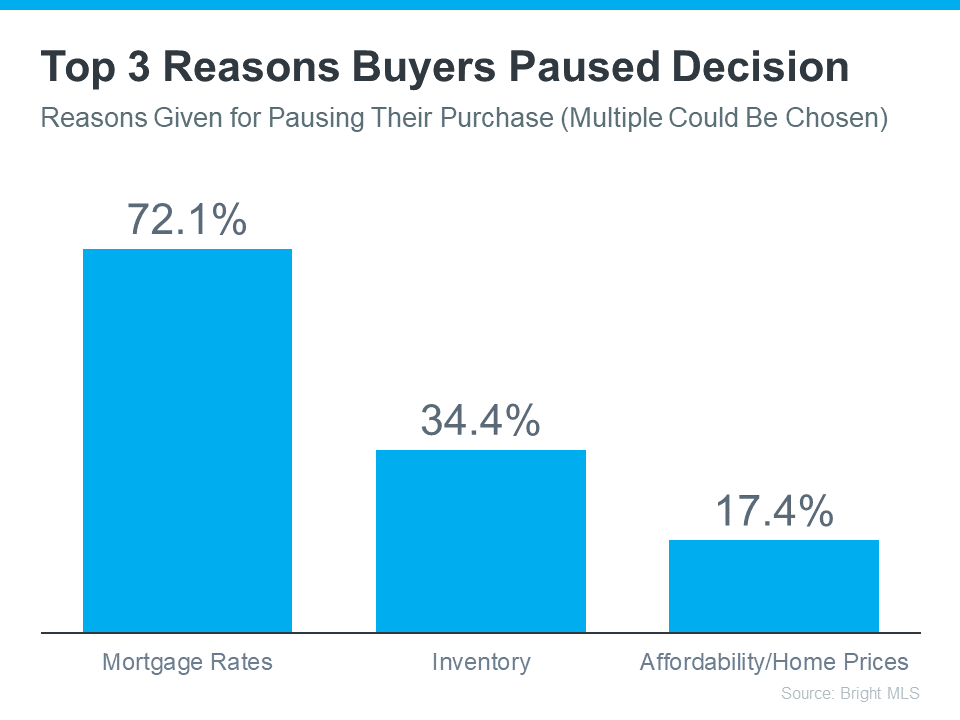

More Buyers Will Be Coming to the Market

According to data from Bright MLS, the top reason buyers have been waiting to take the plunge into homeownership is high mortgage rates (see graph below):

Lower mortgage rates mean buyers can potentially save money on their home loans, making the prospect of purchasing a home more attractive and affordable. Now that rates are easing, more buyers are likely to feel they’re ready to jump back into the market and make their move. And more buyers mean more demand for your house.

Bottom Line

If you’ve been waiting to sell because you didn’t want to take on a larger mortgage rate or you thought buyers weren’t out there, the recent decline in mortgage rates may be your sign it’s time to move. When you’re ready, let’s connect.

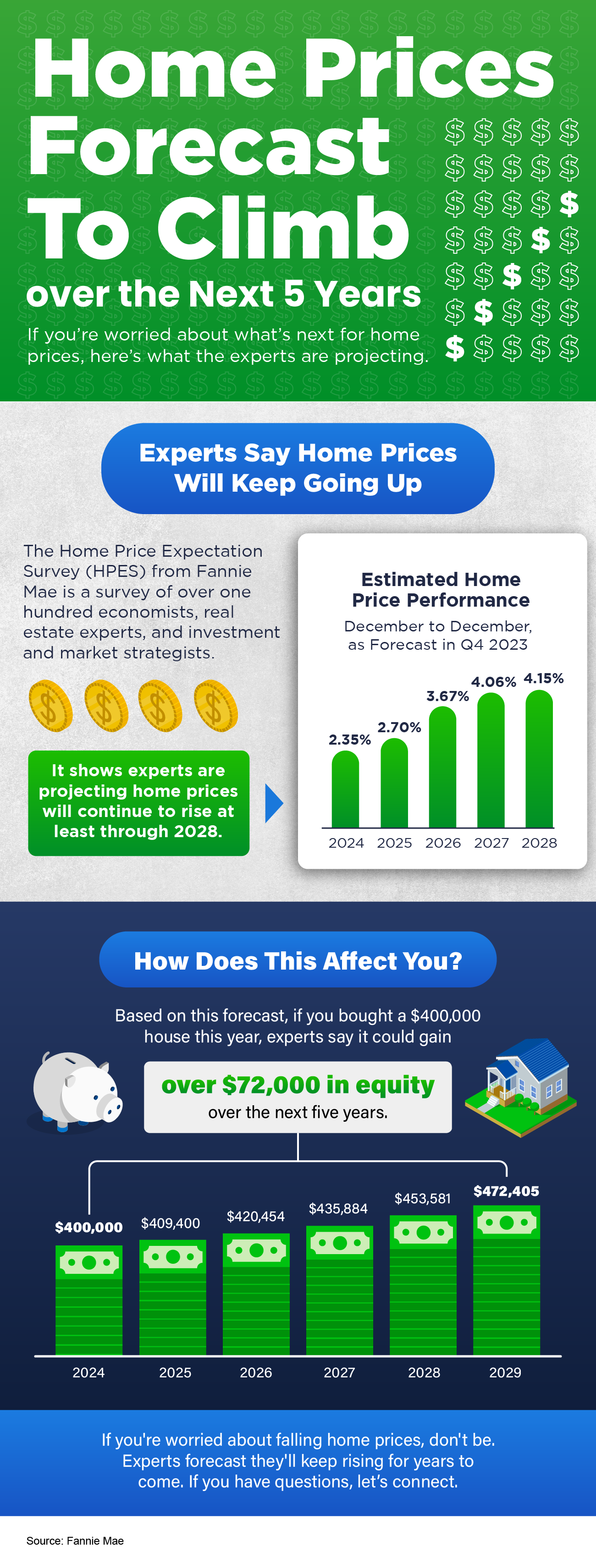

Home Prices Forecast To Climb over the Next 5 Years [INFOGRAPHIC]

Some Highlights

If you’re worried about what’s next for home prices, know the HPES shows experts are projecting they’ll continue to rise at least through 2028.

Based on that forecast, if you bought a $400,000 house this year, experts say it could gain over $72,000 in equity over the next five years.

If you’re worried about falling home prices, don’t be. Many experts forecast they’ll keep rising for years to come. If you have questions, let’s connect.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link